If you're a bank, fintech, or financial institution eyeing East Africa, there's one question worth asking: how did mobile money become the backbone of finance in Uganda and Kenya? The answer is more than a timeline—it's a strategic case study on two markets that took different routes to solve the same problem: financial access at scale.

Uganda and Kenya now process over $110 billion annually in mobile money transactions. Wallets are no longer just an optional payment method when you run out of cash; they’re essential to life and commerce. Yet, the way each country got here offers wildly different lessons in platform design, agent strategy, pricing, and regulatory influence.

Whether you're comparing Uganda vs. Kenya, wondering about mobile money withdrawal charges in Uganda, or evaluating how to use mobile money in Kenya to serve rural clients, this guide unpacks it all.

You're about to explore what works, what scales, and what’s next.

Let’s dive into the ultimate comparison of mobile money in Uganda and Kenya, so that you can make smarter decisions in your own digital finance journey.

Why Mobile Money in East Africa Matters Now More Than Ever

Mobile money in East Africa has moved beyond the trend. It has become a transformation. For financial businesses like yours, Uganda and Kenya offer two of the most compelling case studies of how mobile wallets can build inclusive economies.

This section breaks down the drivers behind their success stories.

Why Uganda and Kenya lead the fintech race in Africa

Uganda and Kenya are setting the pace for fintech adoption in Africa, and here’s why:

-

High unbanked populations: Over 60% of adults in Uganda and more than 30% in Kenya were unbanked before mobile money took off.

-

First-mover telcos: Safaricom’s M-Pesa in Kenya and MTN Mobile Money in Uganda led with relatable and user-first solutions.

-

Proactive regulation: Both countries embraced central bank frameworks that formalized mobile money operations. This enabled trust and scaling.

These factors created a perfect storm for fintech innovation, where mobile money filled financial service gaps left by traditional banking.

A snapshot of mobile money across East Africa

Kenya: Mobile money transactions hit KES 7.95 trillion (~$49.2 billion) in 2023, which showed deep penetration and value density (Xinhua News Agency).

Uganda: Mobile money transaction volume reached UGX 191.3 trillion (~$51.2 billion) in FY 2022/2023 (Business Focus Report).

GDP impact: In Kenya, mobile money transaction value represents 53% of the country’s GDP. In Uganda, it surpasses 125%, a clear sign that mobile wallets drive most of the country’s economic activity.

Mobile money isn’t just a convenience here; it’s the financial system’s heartbeat. That’s why you, as a financial decision-maker, need to understand how each country’s approach can shape your roadmap.

Evolution of Mobile Money: Uganda vs. Kenya

Kenya started first. Uganda scaled fast. Both became benchmarks. Here’s the breakdown👇

Kenya’s journey: From M-Pesa monopoly to platform powerhouse

-

M-Pesa launched a mobile money platform in 2007. It solved one problem: safe remittance

-

It evolved into a full-stack platform with loans, savings, bill payments, merchant tools

-

Competition from banks like Equity Bank and regulatory moves ended agent exclusivity, sparking innovation

-

M-Pesa API (Daraja) opened the ecosystem to developers, which helped in the rise of mobile money apps in Kenya

Uganda’s story: Fast follower, nimble innovator

-

MTN and Airtel launched mobile money around 2009–2010

-

The 2020 National Payments Systems Act brought structure, licenses, and consumer protection

-

Uganda became transaction-dense rather than value-heavy: lots of micropayments, lots of users

-

Uganda mobile money apps are still evolving but have high adoption on feature phones via USSD

Mobile Money Growth Metrics: Who Leads Where?

If you're evaluating market potential or considering expansion strategies, user growth and transaction dynamics are where the story becomes actionable.

Uganda and Kenya are both powerhouses, but the way users interact with mobile money platforms is very different.

User base evolution (2010–2025): Penetration and demographic shifts

-

Kenya has reached near-saturation: ~79% of adults use mobile money regularly. The growth is now more horizontal, i.e. expanding features and increasing use per user.

-

Uganda shows strong uptake with 42M+ registered mobile money accounts and over 25M active users. That’s more than half of its population actively transacting on mobile.

-

Both countries are seeing massive traction in rural adoption, female users leveraging wallets for savings, and youth-driven digital finance use cases.

Where Kenya offers lessons in maturity and ecosystem layering, Uganda presents untapped segments ripe for targeted growth, especially in agriculture, community savings, and informal retail.

Transaction volumes & values: Big volumes vs micro-movements

| Metric | Kenya | Uganda |

|---|---|---|

| Annual transaction value | $67B | $50B |

| Annual transaction volume | ~3B | 5.8B+ |

| Avg. transaction size | $22 | ~$9 |

The insight?

In Uganda, high transaction frequency is a trust signal and a monetization opportunity, especially for services like micro-loans and fee-free utility payments.

In Kenya, depth of service matters more: users are ready for wealth management, SME credit, and digital tax payments.

Together, these numbers tell you where to double down: volume-focused UX in Uganda, value-focused innovation in Kenya.

Pricing & Fees: The True Cost of Convenience

Mobile money adoption was about financial access before. But now it’s also about affordability.

Understanding how fees, transaction caps, and tax policies impact the user journey is essential for any business planning to grow in these markets.

Mobile money charges in Uganda: Fees, withdrawal limits, and taxes

-

Uganda applies a 0.5% mobile money tax on withdrawals, in addition to standard provider fees.

-

These costs make micro-transactions more expensive, especially for users who transact multiple times a day.

-

Providers typically cap daily withdrawals at UGX 5 million, but limits may vary based on customer tier and KYC level.

-

Airtel Money and MTN Mobile Money Uganda offer tier-based fee structures—e.g., a UGX 5,000 withdrawal may cost UGX 500–1,000 depending on provider.

For businesses offering mobile money business in Uganda, pricing sensitivity is key. Building fee optimization into your design like bundling transactions or enabling wallet savings can significantly boost retention in cost-conscious user segments.

Mobile money fees in Kenya: Transaction caps and pricing trends

-

Kenya enforces tiered pricing, but the Central Bank of Kenya (CBK) eliminated off-net fees to promote interoperability.

-

The current daily cap is KES 500,000, with a KES 250,000 per transaction limit.

-

Services like M-Pesa now offer fee-free person-to-person transfers up to a certain threshold, especially during regulatory promotions.

-

Merchant payments via Lipa na M-Pesa are increasingly free for the customer, shifting fees to the merchant side.

For banks and fintechs designing mobile money services in Kenya, pricing innovation and transparency are dealmakers.

The more you can simplify cost structures and reduce user anxiety around hidden charges, the more likely you are to see increased transaction velocity and trust.

All in all, fee structures are not just cost centers; they’re product levers. Use them wisely.

Regulatory Infrastructure: Who’s Winning the Long Game?

Regulation can either accelerate or obstruct innovation. In East Africa, Uganda and Kenya have treated mobile money as a national priority—each shaping the ecosystem through a distinct approach. Here’s how their regulatory environments are influencing long-term fintech success.

Kenya’s regulation: Organic evolution to active governance

-

The Central Bank of Kenya (CBK) played a pivotal role by gradually introducing mobile money regulations without stifling early growth.

-

CBK mandated segregated trust accounts, ensuring mobile money funds were fully backed and secure.

-

To address competition, the Competition Authority of Kenya eliminated agent exclusivity, forcing Safaricom to open its M-Pesa network to rival services like Airtel Money and Equitel.

-

CBK’s 2022–2025 National Payments Strategy emphasizes interoperability, open APIs, and real-time settlement frameworks.

-

M-Pesa-to-bank and bank-to-wallet integrations now support a broader digital finance ecosystem, fostering a more inclusive financial landscape.

Kenya’s regulatory path shows how progressive oversight can unleash private-sector innovation while maintaining systemic trust and competition.

Uganda’s playbook: Structured, inclusive, and fintech-friendly

-

Uganda took a more structured approach with the National Payments Systems Act (2020), which brought telco-operated mobile money services under formal financial regulation.

-

Under this law, providers like MTN Uganda had to spin off mobile money into a regulated subsidiary, MTN Mobile Money Uganda Ltd., licensed by the Bank of Uganda.

-

The law mandates strong KYC, liquidity, and consumer protection standards.

-

Most importantly, Uganda is building the BNPS (Bank of Uganda National Payments Switch), a centralized system to enable seamless wallet-to-wallet and wallet-to-bank transactions, regardless of provider.

This central infrastructure approach is enabling the country to leap ahead in wallet interoperability, cross-platform fund flows, and financial inclusion.

Both nations illustrate that strong regulation isn’t about control; it’s about creating a fair, scalable playground for innovation. For businesses like yours, this means more stable APIs, secure fund flow mechanics, and stronger compliance frameworks to build on.

Technology Infrastructure: The Engine Behind the Wallet

Mobile money adoption follows access. Technological infrastructure for it sets the speed limit on how this mobile money system will work. Here’s the insights:

Connectivity, smartphones, and app-readiness:

Kenya: 72% smartphone penetration, widespread 4G/5G rollout

Uganda: ~36% smartphone users, feature phones still dominate

This affects how people access mobile money apps in both countries

If you’re designing mobile money apps in Kenya, go native and app-first. In Uganda, prioritize USSD and SMS.

Agent networks: Rural trust, liquidity, and financial inclusion:

-

Kenya: ~300K active agents

-

Uganda: ~480K mobile money agents

-

Mobile money agent network performance directly impacts cash accessibility

-

Agent training, liquidity tools, and territory management are non-negotiables for financial businesses like yours.

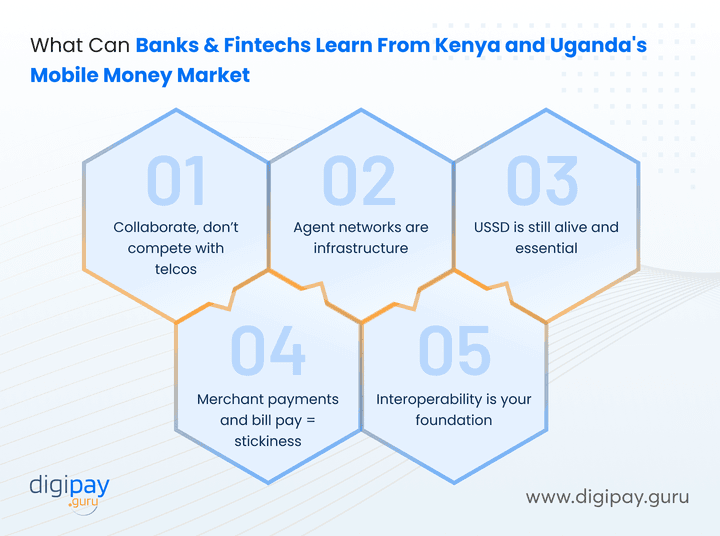

What Can Banks & Fintechs Learn From Both?

If you’re building, scaling, or optimizing mobile money services, these are your takeaways.

5 lessons from Kenya and Uganda’s mobile money evolution

-

Collaborate, don’t compete with telcos: Kenya’s Equity Bank didn’t try to replace M-Pesa, but it integrated with it. In Uganda, financial institutions leverage MTN Mobile Money and Airtel Money rails to expand reach, not replace infrastructure.

-

Agent networks are infrastructure: You can't build a mobile money business without reliable last-mile delivery. Agents are more than access points. They’re brand ambassadors, liquidity providers, and trust enablers. In Uganda especially, agent density enables high transaction frequency.

-

USSD is still alive—and essential: In Uganda, with only ~36% smartphone penetration, USSD remains the most inclusive tech layer. Banks and fintechs like yours need to design low-data or zero-data user experiences to scale rural outreach.

-

Merchant payments and bill pay = stickiness: Kenya’s success with Lipa na M-Pesa shows that recurring, everyday payments build habit loops. Enabling utility payments, school fees, and micro-insurance premiums via mobile money increases both frequency and lifetime value per user.

-

Interoperability isn’t optional; it's your foundation: Cross-wallet and wallet-to-bank interoperability is no longer a future roadmap item. It’s a basic expectation. Institutions that plan around a single channel or closed loop will lose relevance fast.

Whether you’re analyzing the fintech ecosystem in Kenya or exploring mobile banking trends in East Africa, the lesson is the same: scale is strategy.

The Road Ahead: Growth Gaps and Opportunities

As discussed so far, mobile money adoption is high. Now it’s time to unlock value, lower friction, and go regional.

What’s next for mobile money in Uganda and Kenya

-

Add wallet-native financial services (savings, credit, insurance)

-

Push mobile point-of-sale adoption for SMEs and micro-retailers

-

Enable cross-border mobile money transfer via regional switches

-

Consider smart incentives for agents and merchants to sustain transaction velocity

The next phase is about ecosystem depth, not just reach.

Building Scalable Mobile Money Platforms for the Future

Scaling mobile money services isn’t just about launching an app. It’s about building infrastructure that’s future-proof.

Why platform flexibility and scalability matter now more than ever

-

Support for wallet-to-bank interoperability and real-time APIs

-

Built-in modules for KYC, AML, and agent management

-

Resilient, cloud-native platforms with custom UI/UX flexibility

-

Enables digital onboarding, transaction insights, and regulatory compliance from Day 1

If you're in a fast-moving market like Uganda or Kenya, legacy systems will hold you back. Flexibility is your growth engine.

How DigiPay.Guru Empowers Institutions to Scale Mobile Money

Scaling mobile money in Africa is not about going digital. It’s about going local, secure, and scalable. At DigiPay.Guru, we understand the complexity of delivering trusted financial services across fragmented networks, diverse devices, and demanding compliance standards.

We’ve worked with leading banks, financial institutions, fintech startups, and other financial businesses across Uganda, Kenya, and other parts of Africa to build mobile money solutions that don’t just lead but transform the market.

What we offer and why it matters to you:

-

Modular mobile wallet architecture that supports P2P transfers, bill payments, merchant payments, savings, loans, and cashback configurable to match local behavior.

-

Multi-agent management with tools to monitor float, enable onboarding, and provide liquidity alerts in real-time, crucial for both Uganda’s rural networks and Kenya’s urban saturation.

-

Built-in fraud detection, audit trails, and AML/CFT compliance workflows that adapt to regional regulations like Uganda’s NPS Act and Kenya’s CBK mandates.

-

Open APIs, fast deployment timelines, and flexible integrations, from mobile apps to USSD to how to top up wallets or embed it into your existing banking core.

You don’t just need a platform. You need a growth partner who understands the business, customers, the pain points, and the pace of these markets.

FAQ's

Kenya has a higher percentage of its population using mobile money. Around 79% of adults are active users. However, Uganda leads in total transaction volume, with over 5.8 billion transactions annually.

Uganda has 42 million registered accounts and 25 million active users, which reflects a larger absolute user base. The difference? Kenya is more value-dense per user, while Uganda is more transaction-dense.

In Uganda, users pay a 0.5% tax on all mobile money withdrawals, plus standard provider fees (typically UGX 500–1,000 depending on transaction size and provider). Daily withdrawal limits are capped around UGX 5 million.

In Kenya, pricing is tiered by transaction value. Daily limits are higher, KES 500,000 per day, with KES 250,000 per transaction. Kenya also benefits from interoperability policies that removed off-net fees, lowering user costs.

Businesses entering these markets should design pricing experiences that account for these structural differences.

-

In Kenya, M-Pesa remains the dominant app, followed by Equitel, Airtel Money, and apps that integrate with wallet rails (like Tala or KCB Mobile).

-

In Uganda, MTN Mobile Money Uganda and Airtel Money Uganda lead the space. Apps are increasingly gaining ground, but USSD remains a key access channel, especially in rural and low-bandwidth areas.

Fintechs should ensure mobile money solutions are both app-ready and USSD-accessible in Uganda.

Yes. Both countries have regulatory frameworks in place to ensure mobile money safety. In Kenya, the Central Bank mandates segregated trust accounts, secure KYC protocols, and data protection. In Uganda, the National Payments Systems Act ensures licensed operations, transaction audits, and consumer safeguards.

For businesses like yours, aligning with these frameworks is essential not just for compliance, but also for customer trust and platform integrity.

Yes. With growing success. In Kenya, CBK has mandated interoperability across wallets, so users can send and receive money across M-Pesa, Airtel Money, and Equitel. In Uganda, the government is building the Bank of Uganda National Payments Switch (BNPS) to enable real-time, cross-network transfers.

This means your mobile money solution must be interoperability-ready to stay relevant and future-proof.